Will Solana’s “double disinflation” overhaul choke DeFi yields or protect SOL long term?

Solana’s monetary policy is back under the spotlight after a fresh proposal to sharply slow token emissions. The plan, dubbed the “Double Disinflation Rate” and formally introduced as Solana Improvement Document (SIMD)-0411, has split opinion between DeFi yield seekers and long‑term network supporters.

At its core, the proposal aims to make SOL a scarcer asset over time by accelerating the rate at which inflation falls. That directly affects staking yields and, by extension, the attractiveness of Solana‑based DeFi strategies built on liquid staking tokens (LSTs).

What is Solana’s “double disinflation” plan?

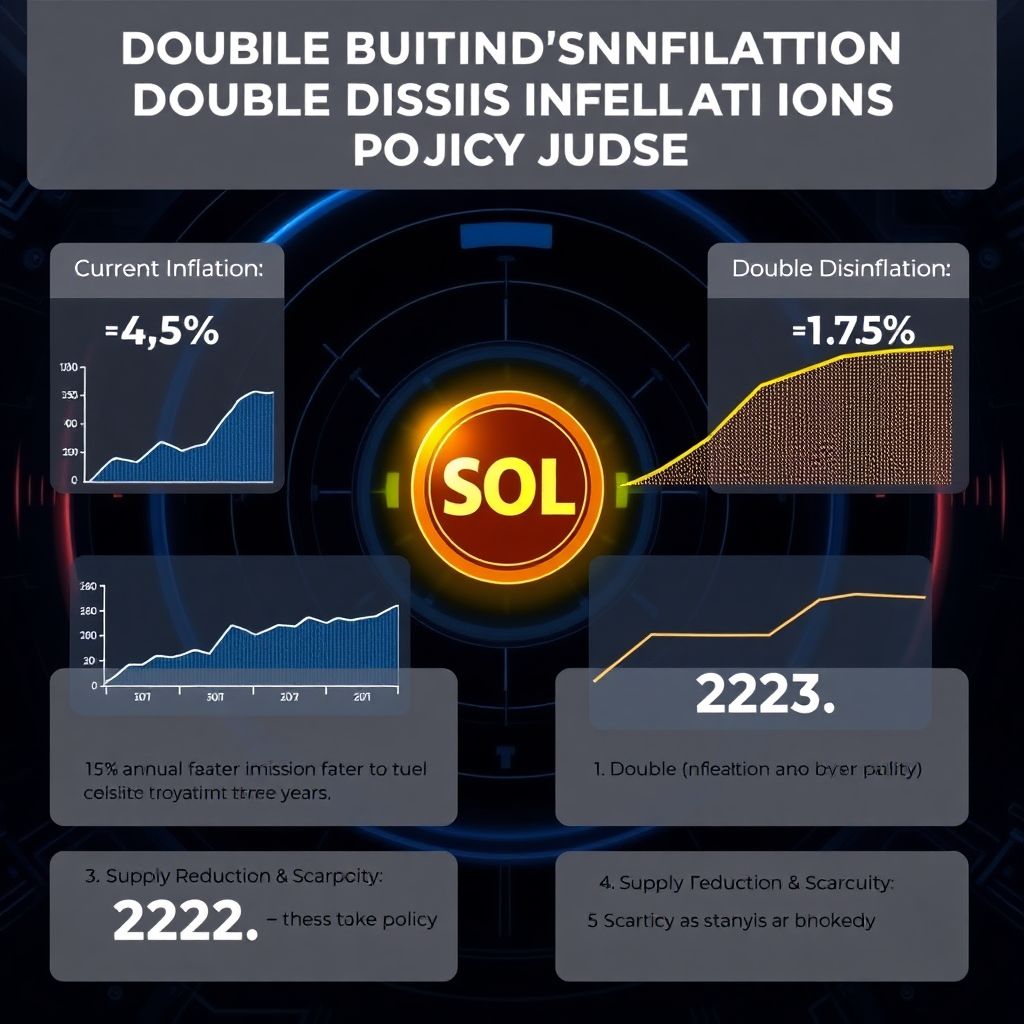

Solana currently operates with an annual inflation rate of about 4.5%. This inflation predominantly comes from staking rewards issued to validators and delegators who secure the network. Alongside that, the protocol uses a “disinflation rate” of 15% per year — essentially, a built‑in schedule that gradually lowers inflation over time.

Under the status quo, if the disinflation rate remains fixed at 15%, Solana’s annual inflation would be expected to decline from 4.5% to roughly 2.5% over the next three years.

SIMD‑0411 proposes to double this disinflation rate from 15% to 30%. That means inflation would fall much faster. Instead of heading toward 2.5% over three years, the annual inflation is projected to slide to just 1.5% over the same period.

This is why the plan is often described as “double disinflation”: the pace at which inflation shrinks is being doubled, leading to a much steeper decline in new SOL entering the market.

How much SOL could be removed from the schedule?

Backers of the proposal highlight the cumulative effect of such a change. According to the SIMD‑0411 projections, roughly 22.3 million SOL would be cut from the inflation schedule over a six‑year period if the change is approved.

At current prices referenced in the proposal, that reduction represents around 2.9 billion dollars’ worth of potential supply that would never hit the market as staking rewards. In other words, it is a sizeable chunk of future sell pressure that could be avoided.

The logic is straightforward: fewer new tokens minted means less SOL routinely entering circulation via rewards, and therefore less structural incentive for stakers to sell those tokens to cover costs or lock in profit.

Why some DeFi participants are worried

While the plan may sound attractive from a scarcity and long‑term value perspective, it comes with an obvious trade‑off: lower inflation generally implies lower staking yields, at least in nominal terms.

Analyst Ignas, a vocal critic of the timing and structure of the proposal, emphasized that DeFi yields tied to Solana’s staking economy could become far less compelling in the short run. This is particularly relevant for liquid staking tokens such as jupSOL, which bundle staking rewards into a liquid asset used across Solana’s DeFi ecosystem.

Ignas argued that, if nominal staking rates drop too quickly, the risk‑adjusted return for holding LSTs — and even SOL itself — could become unattractive compared to other yield opportunities. He acknowledged that, from a long‑term perspective, lowering inflation is likely the sound move for the health of SOL’s price chart. However, he also underscored that the near‑term hit to yields may cause capital to rotate out of Solana’s DeFi sector.

In effect, the concern is that aggressive disinflation might inadvertently cool DeFi activity right when many ecosystems are competing to attract liquidity with high yields.

Mert Mumtaz: plug the “leaky bucket”

On the other side of the debate, Mert Mumtaz, founder of Helius Labs, has strongly endorsed SIMD‑0411. He frames the current inflation schedule as a “leaky bucket,” where valuable SOL is continuously minted and then sold into the market, often for reasons unrelated to network growth.

A large portion of newly issued SOL ends up being sold by stakers and validators to pay taxes or operational expenses. Mumtaz argues that reducing emissions is effectively a way of stopping the network from over‑subsidizing these costs at the expense of long‑term holders.

From this angle, cutting inflation is not about starving validators or undermining security, but about eliminating unnecessary dilution. Mumtaz maintains that the proposed reduction is modest in the short term while saving the network from millions of dollars’ worth of excessive emissions over time.

He also stresses that SIMD‑0411 is far less drastic than prior attempts to slash inflation, positioning it as a balanced compromise between protecting yields today and preserving value tomorrow.

How does this differ from the previous 80% cut proposal?

The question of inflation is not new for Solana. Earlier in the year, another improvement document, SIMD‑228, proposed an aggressive 80% cut to the inflation rate. That plan was seen as a radical step that would have significantly damaged staking rewards almost overnight.

The community ultimately pushed back on SIMD‑228, largely out of concern that such a deep reduction could harm validator economics and risk network security, while making staking far less appealing.

In contrast, SIMD‑0411 aims to be more incremental. Instead of slashing the headline inflation number immediately, it accelerates the existing process by which inflation decays each year. Proponents say this approach smooths the adjustment curve, reducing shock to participants who rely on staking returns, while still moving decisively toward a leaner issuance model.

Despite that more measured tone, short‑term critics argue that even a softer approach can still depress yields enough to matter for DeFi liquidity providers, at least during the transition period.

What does it mean for Solana DeFi yields?

In the near term, DeFi yields on Solana that are directly or indirectly tied to staking rewards are likely to compress if SIMD‑0411 passes. This particularly affects:

– Liquid staking tokens (LSTs) like jupSOL, which pass through staking rewards to holders.

– Lending protocols where LSTs are used as collateral or interest‑bearing assets.

– Yield‑farming strategies that use LSTs in liquidity pools to amplify returns.

As the base staking rate falls with lower inflation, the expected yield from holding these tokens in their simplest form will also decrease. DeFi protocols may attempt to offset this decline through incentives, higher leverage, or new tokenomics, but those come with additional risk.

Over time, however, if reduced inflation leads to a stronger and more stable SOL price, total returns (price appreciation plus yield) could remain competitive or even improve. From an investor’s perspective, a lower nominal yield on a more valuable, less diluted asset can be preferable to a higher yield on an asset that is constantly being inflated.

The challenge is the interim period, when yields drop before any potential price benefits from lower inflation are fully realized. That gap is where DeFi farmers may feel the squeeze most acutely.

Can lower inflation coexist with strong DeFi growth?

The tension between inflation policy and DeFi growth is not unique to Solana. Other networks have gone through similar debates: how to balance generous staking rewards that attract capital with long‑term sustainability and scarcity.

In principle, a lower inflation regime does not have to be hostile to DeFi. If the network continues to scale, transaction volumes increase, and fee revenues grow, validators and stakers can gradually rely more on fees rather than pure emissions. In such a scenario, yields become tied to actual network usage rather than inflation subsidies.

For Solana, this would mean that DeFi yields could increasingly be driven by real economic activity — trading fees, borrowing costs, liquidations, and protocol revenue — instead of being primarily funded by new token issuance. That shift would likely take time and requires robust, sustained on‑chain usage.

Project teams may also adapt their incentive structures, building more complex, multi‑token reward schemes or profit‑sharing models to keep yields attractive even as base staking returns trend lower.

Impact on validators and network security

Another key question is whether a faster fall in inflation might undermine validator economics and, by extension, network security. Validators invest in hardware, infrastructure, and operations, counting on staking rewards to make the business viable.

If rewards fall too quickly without a compensating rise in SOL’s price or network fee revenue, some marginal validators could face pressure, potentially leading to more centralization as only the largest or most efficient operators remain profitable.

Supporters of SIMD‑0411 argue that the cut is “non‑adverse” and designed to avoid this scenario. Because the disinflation increase is gradual and the starting inflation rate is relatively moderate at 4.5%, the expectation is that validators will have time to adjust. If SOL’s price benefits from lower dilution, the dollar value of rewards may hold up even as the number of tokens paid out declines.

Moreover, as long as Solana continues to attract applications and users, rising fee income can gradually play a larger role in compensating validators, reducing dependence on inflation‑funded rewards over the long haul.

What does this mean for SOL holders?

For existing SOL holders, the proposal is broadly favorable from a dilution standpoint. Less inflation means less new supply competing with current holdings, which tends to be supportive for price over multi‑year horizons, all else being equal.

However, investors who rely heavily on staking yields as an income stream will need to reassess their strategies. Portfolio allocations optimized for a 4.5% inflation regime may not make the same sense in a world where inflation heads toward 1.5% within three years.

Some may seek higher yields in more speculative DeFi strategies, accepting greater risk. Others might reduce exposure to yield‑farming altogether and adopt a longer‑term, lower‑yield but potentially more secure approach, betting that scarcer SOL will reward patience.

In any case, the proposal forces market participants to think beyond raw APYs and pay more attention to total return, risk profiles, and time horizons.

Market context: SOL’s price backdrop

At the time referenced in the original discussion, SOL was trading around 129 dollars, roughly 50% below its September peak of 253 dollars. That drawdown provides a backdrop to the urgency around tokenomics reforms.

Supporters of the double disinflation plan see a leaner issuance schedule as a key ingredient in stabilizing Solana’s price structure and restoring confidence among longer‑term investors. Critics, however, worry that dampening yields too quickly during a price slump could compound outflows from DeFi just when the ecosystem needs liquidity and engagement.

This tension between short‑term DeFi competitiveness and long‑term monetary discipline underpins much of the debate around SIMD‑0411.

How the decision will be made

The fate of the double disinflation plan will ultimately be decided by Solana’s governance process. Stakeholders will weigh the projected reduction in future sell pressure and improved long‑term tokenomics against the immediate impact on staking returns and DeFi incentives.

While the exact voting mechanics and timelines are subject to the network’s governance standards, the broader question is strategic: should Solana prioritize being a high‑yield DeFi playground today, or move more decisively toward being a scarcer, institutionally attractive asset with a conservative issuance schedule?

The answer will shape not only returns for yield farmers in the coming years but also the narrative around SOL as a long‑term investment.

Weighing the trade‑offs

The double disinflation proposal highlights a classic crypto dilemma: sustainable tokenomics versus aggressive growth incentives. On one side are DeFi users who depend on juicy yields to justify the risks they take; on the other, builders and long‑term holders who want to see SOL evolve into a robust, non‑inflationary asset.

SIMD‑0411 attempts to thread the needle by adjusting existing parameters rather than imposing a sudden, drastic overhaul. Even so, it will likely compress yields enough to be felt across Solana’s DeFi ecosystem in the short term.

Whether that short‑term discomfort pays off in the form of a stronger, more resilient SOL economy will depend on how quickly the network can convert lower inflation into higher confidence, greater adoption, and ultimately, more organic, usage‑driven yields. As the vote approaches, both DeFi farmers and long‑horizon investors will be watching closely, each with very different priorities at stake.